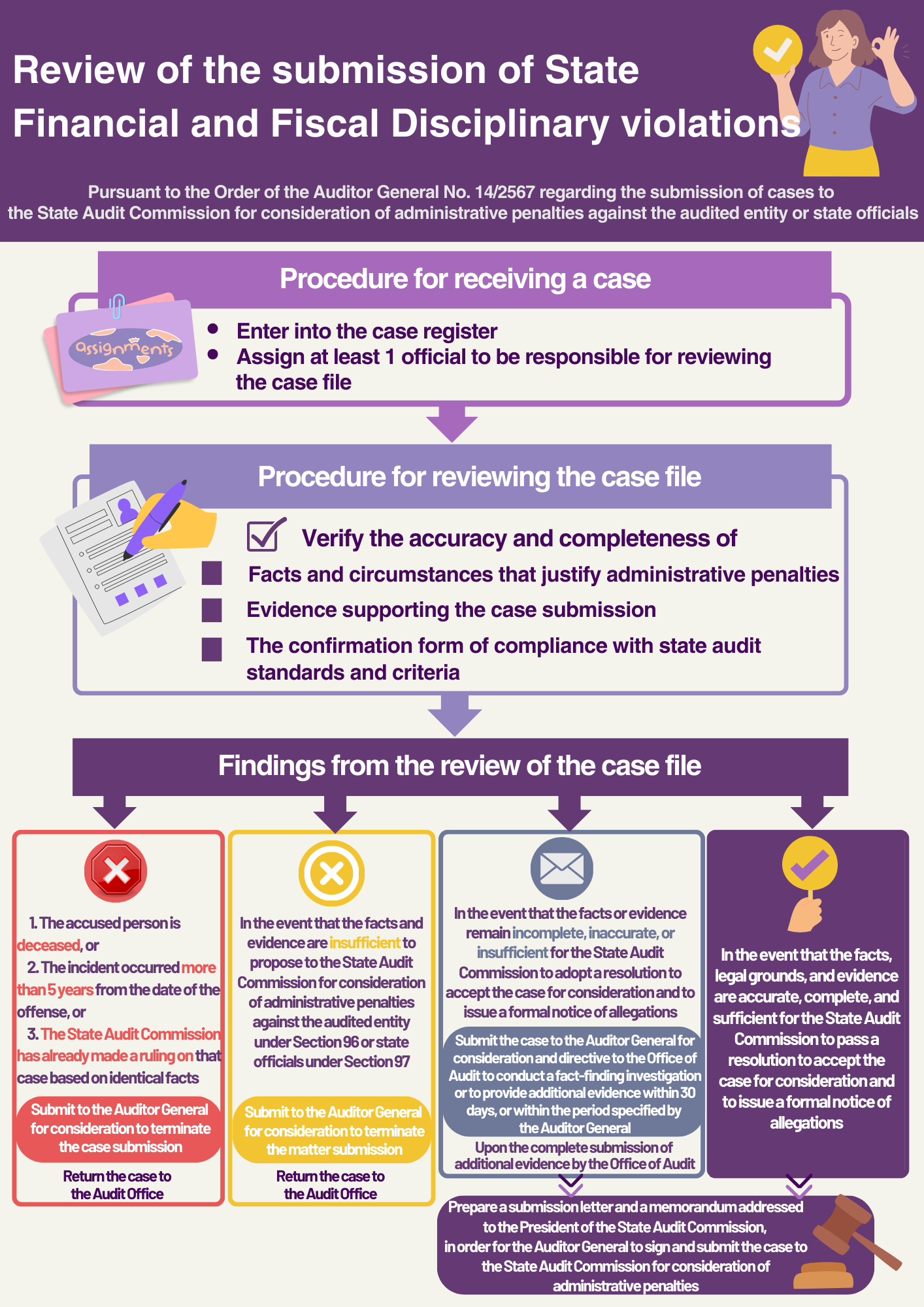

The Procedures for reviewing of the submission of the State Financial and Fiscal Discipline offense case

When the Auditor General receives a case file pertaining to state financial and fiscal disciplinary violations from the Audit Office, the Auditor General shall assign the Office of Financial and Fiscal Discipline to review the case file and prepare a formal submission document. This procedure complies with the guidelines for submission of state financial and fiscal disciplinary violation cases issued pursuant to the Auditor General's Order No. 14/2567 dated October 25, 2024, regarding "The Submission of Cases to the State Audit Commission for Consideration of Administrative Penalties for Audited Entities or State Officials", which has established the following review procedures and guidelines:

1. Procedure for Case Receipt and Case File Review

Upon receipt of the case file along with the submission form from the Auditor General, the Director of the Office of Financial and Fiscal Discipline shall proceed as follows:

1.1 Ensure that the case is recorded in the case registry for control and monitoring purposes, in order to preclude the financial and fiscal disciplinary case from exceeding the statutory limitation period of 5 years from the date the offense was committed.

1.2 Assign the case to the officials of the Office of Financial and Fiscal Discipline who shall be responsible for examining and reviewing the case file.

- To verify the accuracy, completeness, and sufficiency of the facts and evidence in the case file, in order to determine whether they are adequate for the State Audit Commission to pass a resolution to accept the case for consideration and to issue a formal notification of allegations.

- To verify the accuracy, completeness, and integrity of the Confirmation Form of Compliance with State Audit Standards and Criteria.

2. The findings from the case review shall be classified for consideration as follows:

2.1 In the event that the Office of Financial and Fiscal Discipline has reviewed the case and the preliminary facts indicate any of the following circumstances:

- The accused person is deceased, or

- The incident occurred more than 5 years from the date of the offense, or

- The State Audit Commission has already made a ruling on that case based on identical facts

The case officer shall consider submitting an opinion through the hierarchical chain of command to the Auditor General for consideration to terminate the submission of the state financial and fiscal disciplinary violation case, and to return the case to the Audit Office.

2.2 In the event that the Office of Financial and Fiscal Discipline has reviewed the case file and finds that there are insufficient facts or evidence to submit the case to the State Audit Commission for consideration of administrative penalties against the auditee under Section 96 or state officials under Section 97 of the Organic Act on State Audit B.E. 2561 (2018).

The case officer shall consider submitting an opinion through the hierarchical chain of command to the Auditor General for consideration of terminating the submission of the state financial and fiscal disciplinary violation case and returning the case to the Audit Office.

2.3 In the event that the Office of Financial Discipline has reviewed the case file and finds that the facts or evidence remain incomplete, inaccurate, or insufficient for the State Audit Commission to pass a resolution to accept the case for consideration and issue a formal notification of allegations, and additional facts or evidence are required to ensure completeness, the case officer shall consider submitting an opinion through the hierarchical chain of command to the Auditor General for consideration to direct the Deputy Auditor General or the Director of the Audit Office who submitted the case to provide additional facts or submit supplementary evidence within 30 days from the date of receipt, or within a period specified by the Auditor General.

2.4 In the event that the Office of Financial Discipline has reviewed the case file and finds that the facts and evidence are accurate, complete, and sufficient for the State Audit Commission to pass a resolution to accept the case for consideration and issue a formal notification of allegations, the case officer shall prepare a submission letter and a memorandum addressed to the President of the State Audit Commission, for the Auditor General to sign and submit the case to the State Audit Commission for consideration of administrative penalties against the auditee under Section 96 or state officials under Section 97 of the Organic Act on State Audit B.E. 2561 (2018).

Home